Table of Contents

The rise of Decentralized Finance (DeFi) and decentralization has established Web3 as the future of the internet. This new blockchain-based ecosystem envisions a decentralized web where users have greater control over their data and assets. To access this new realm, Web3 wallets serve as a crucial gateway. These digital wallets enable users to store, send, receive, and interact with cryptocurrencies, non-fungible tokens (NFTs), and decentralized applications (DApps).

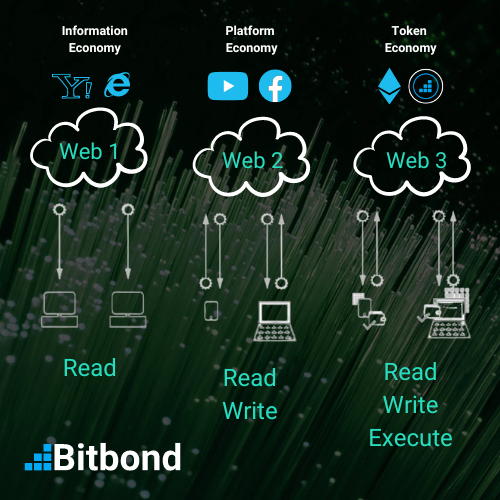

Web1.0 to Web3.0: A Brief History

To understand Web3, it’s essential to grasp the evolution of the internet. Web1.0, the first iteration, characterized by static websites and read-only access, paved the way for Web2.0, the interactive and user-generated content era. With Web2.0, social media platforms and e-commerce giants emerged, giving rise to centralized control and data privacy concerns. Web3 aims to address these challenges by empowering users with ownership and control over their data and assets.

Berners-Lee had written the three fundamental technologies that became the foundation of the Web 1.0, including the first editor/browser for web pages (WorldWideWeb.app): HTML, URL, HTTP

Web 2.0 describes a paradigm shift in the way the Internet is used. In the last 15 to 20 years, Web 1.0’s soft web pages have been completely replaced by Web 2.0’s interactivity, social connectivity, and user-generated content. Web 2.0 makes it possible for user-generated content to be viewed by millions of people around the world in practically no time. This unprecedented reach has fueled an explosion of this type of content in recent years.

Web 3.0 represents the next iteration or phase of the web/internet evolution. It could potentially be just as disruptive and paradigm shifting as Web 2.0. Web 3.0 builds on the basic concepts of decentralization, openness and increased utility.

In other words:

- Web 1 consisted of read-only access to the internet (web pages, surfing the internet with links).

- Web 2 made reading and writing accessible to internet users as it became more mature (Apps could be used to read and write simultaneously, enabling global interaction virtually between users, but always using a platform acting as a trusted intermediary, e.g social media & e-commerce).

- Web 3 revolutionized the back-end of the internet, as the front end remains the same, it is now possible for anyone to participate in verifying transactions and get rewarded accordingly. Agreements are executed P2P and instantly through smart contracts. A distributed ledger is used as the underlying network guaranteeing safety and security, where connection is facilitated by “wallets”.

Web3 Wallets: Essential Tools for the Decentralized Web

Web3 wallets play a pivotal role in this new ecosystem. They act as digital vaults for storing crypto assets, enabling users to participate in DeFi, purchase NFTs, and interact with DApps. These wallets range from non-custodial wallets, where users hold private keys, to custodial wallets, where a third party manages the keys.

Top Web3 Wallets: A Glimpse into the Ecosystem

Metamask

Metamask wallet is one of the most widely adopted non-custodial web3 wallets in the market. Founded in 2016 by ConsenSys, one of the biggest players in blockchain, crypto, and web3; MetaMask is a software cryptocurrency wallet used to interact with the Ethereum and EVM blockchains. It allows users to access their Ethereum wallet through a browser extension or mobile app. It offers all kinds of access to DeFi services such as staking, DEX, and liquidity pools through interacting with decentralized applications (dApps).

Metamask also launched Metamask Institutional as part of their push strategy to bring all organizations onto web3. With MM institutional, financial institutions can now benefit from top notch custody solutions enabling them with the possibility of accessing DeFi and benefiting from a new range of financial services.

Brave Wallet

Brave wallet is part of the Brave browser project. With its project token BAT, Brave aims to compete with traditional Big Tech companies by providing “online privacy by default” as an added value to users. Their USP is that users can earn rewards while browsing, Brave Rewards gives you the option to view first-party, privacy-protecting ads while you browse (these ads are from the Brave Private Ads network). If you choose to view them, you earn BAT, via the Brave Rewards program.

As they aim to expand their product offering, they are launching Brave Wallet which is still in beta phase. The multi-chain web3 wallet allows users to buy, sell and sway crypto assets and is built directly into the Brave browser. It supports Ethereum, Avalanche, Polygon, BNB Chain, Solana and is planning to introduce support for Bitcoin and other protocols.

You can download Brave on mobile (iOS & Android) or desktop and it is a non-custodial wallet (aka self custody).

Coinbase Wallet

Coinbase Wallet has been developed by Coinbase, one of the largest crypto exchanges. Coinbase Wallet is a non-custodial web3 wallet that enables users to securely store 44,000+ digital assets, interact with decentralized applications, and manage their Ethereum-based NFTs.

Currently, Coinbase Wallet supports the Bitcoin, Ethereum, Binance Smart Chain, Dogecoin, Litecoin, Polygon, Stellar, and Ripple network, as well as numerous Ethereum Layer-2 solutions, such as Arbitrum and Optimism. Users can swap Ethereum- and Polygon-based assets directly within the app’s decentralized exchange feature. Non-Ethereum and Polygon assets can be purchased using the in-app crypto buying option.

Additionally, Coinbase offers custody technology for institutional clients who wish to take part in the rising DeFi market.

Trust Wallet

Trust Wallet was built for convenience, allowing users to accumulate, send, receive, and stake over 1 million cryptocurrencies and non-fungible tokens (NFTs) from their smartphone. New cryptocurrency users will appreciate the simplicity, but may experience problems if their account is compromised.

Trust Wallet is a diverse non-custodial web3 wallet, with support for over 1 million different cryptocurrencies across blockchains managed on a smartphone. Through the app, Trust Wallet users can buy cryptocurrency, send and receive coins, and buy and sell NFTs. Because Trust Wallet primarily works on smartphones, it may be difficult to use it with NFT marketplaces and decentralized exchanges. As a decentralized wallet, customer service is limited to technical issues – users can’t get help recovering secret phrases or PINs to restore access to their currency.

WalletConnect

WalletConnect is an open source protocol for connecting decentralized applications to cryptocurrency wallets. It is a middleware that is used as a bridge between wallets and dapps. WalletConnect is basically a protocol used by many web3 wallets that enables users to easily connect with the many DApps of decentralized finance (DeFi). It can be used on desktop and mobile, simply find the DApp you want to interact with, connect with a QR code or deep link, and you’re good to go. Always remember to disconnect at the end of any session for maximum security.

What’s valuable in using WalletConnect as a service provider, is that it can be integrated within your product in just a few lines of code. Therefore, enabling you with a simple solution to provide access to your platform to an extended set of users without needing to implement different wallets individually.

Gnosis Safe

Gnosis Safe is a smart contract “multisig” wallet running on Ethereum that requires a minimum number of people to approve a transaction before it can occur. If for example you have 3 main stakeholders in your business, you are able to set up the wallet to require approval from all 3 people before the transaction is sent. This assures that no single person could compromise the funds.

Users and organizations can then easily interact with DApps once they are listed among the Gnosis Safe App benefiting from a wide range of financial products made available by DeFi, while maintaining high safety & security standards.

Qredo

Qredo Wallet is a web application that makes digital asset portfolio management fast and secure. It delivers institutional grade secure crypto storage and supports instant peer to peer transfers, and cross-chain swaps.

Built to scale, the Qredo Wallet allows you to control access to digital assets across trusted parties, teams or organizations using simple but powerful roles and access rights. With Qredo Wallet, the private keys aren’t generated to begin with. Instead, Qredo uses the Multi-Party Computation (MPC) architecture. The MPC network signs and validates transactions in a way that replaces the need for individual private keys.

The Qredo Web3 Wallet allows cross-chain swaps of supported assets. All within Qredo, without any withdrawal fees.

Fireblocks

Fireblocks provides digital asset custody infrastructure specialized for financial institutions. Fireblocks combines MPC-CMP with hardware isolation to create a multi-layer security technology. This eliminates a single point of failure and insulates digital assets from cyber-attacks, internal collusion, and human error.

It is basically a Wallet-as-a-Service solution that unifies your digital assets under 1 platform to make the management of assets seamless and compliant for institutional clients.

Dfns

Dfns is a cybersecurity company providing wallet infrastructure for Web3. From institutional banks to fintechs, we enable developer teams with plug-and-play access to digital assets through our secure wallet-as-a-service (WaaS) platform. Dfns is API-first and has been designed with developer experience in mind to maximize programmability and minimize high-touch implementation time.

Dfns is powered by an MPC-based decentralized key management network that eliminates all single points of failure and trust through the wallet lifecycle and provides built-in recovery mechanisms as well as bank-grade error-and-attack-resilience leveraging Tier 3+/4 data center partners.

Founded in 2020 in Paris, Dfns is a SOC-certified company incubated at Techstars, Station F (awarded Future 40in 2021) and recognized DeepTech by the French Ministry of Economy and Innovation.

Binance Wallet

The Binance wallet is an exchange-based way of storing your cryptocurrencies. As opposed to that, the Trust wallet is also a web3 wallet that belongs to Binance, but is a completely different, dedicated product. Whether you were to use the Binance wallet app or the web browser version of the wallet, it’ll have the full functionality of the platform integrated into it. Among other things, this functionality involves that of a crypto exchange.

Binance is among the largest crypto-exchanges in the world.

It is a non-custodial wallet, supporting a variety of cryptocurrencies. It has cold storage capacities and has other safety features such as multisig and 2FA. Available as an app or browser extension, it is a Crypto Wallet for Binance Chain, Binance Smart Chain and Ethereum

Crypto.com

Crypto.com DeFi Wallet is a non-custodial web3 wallet that allows users to safely store their crypto in a highly secure environment with their private keys. Users can send and receive up to 78 cryptocurrencies like Bitcoin(BTC), Ethereum(ETH), DeFi coins like Uniswap(UNI), Compound(COMP), yearn.finance(YFI), stablecoins and other ERC20 tokens. The Crypto.com DeFi Wallet is available for both Android or iOS devices. If you are using the Crypto.com App, you can download and connect the Crypto.com DeFi Wallet to easily access the diverse crypto financial services offered by Crypto.com.

The Crypto.com DeFi Wallet is also Crypto.com’s first touch on the DeFi (Decentralized Finance) arena. It offers users a simple and secure way to access and explore DeFi projects. Crypto.com DeFi Wallet is integrated with WalletConnect, allowing users to connect with DeFi Swap and other DApps by scanning the QR Code.

Ledger Live

Ledger is known for their hardware wallets. The Ledger Live app is available on both Google Play and App Store. On the Ledger Nano X wallet, the app is supported on Android 7+ and iOS 9+ using a Bluetooth connection. On the Ledger Nano S, the app is supported on Android 7+ using a USB cable. You can also download the Ledger desktop app on your Windows, macOS and Linux operating systems.

With its simple and clear interface, Ledger Live lets you enjoy the simplicity of monitoring your real-time balance and managing all your transactions. Overall, Ledger is a reliable and highly-secure web3 wallet that combines a secure element and a proprietary OS designed to protect your crypto assets. If your preferred crypto isn’t among the over 1,500 already-supported crypto assets, you can use 1 of the more than 50 compatible external wallets to manage your crypto.

MyEtherWallet

MyEtherWallet (MEW) is a market-leading Ethereum wallet that enables users to store Ether (ETH), ERC-20 tokens, and non-fungible tokens (NFTs) using the multi-platform web3 wallet. Moreover, MEW users can buy, sell, swap, and exchange cryptocurrency within the wallet’s interface.

The open-source wallet also allows users to interact with smart contracts and decentralized applications (DApps) to provide full access to the Ethereum ecosystem.

MyCrypto

MyCrypto combines the core security and privacy features inherent to cryptocurrency and blockchains with a visually appealing, easy-to-use interface. Optimized for use with Ethereum, the app gives new users an online banking-style platform, while experienced users can use it to operate with more privacy and create offline storage wallets.

Exodus

Exodus is a multi-currency web3 wallet that I usually recommend as an entry wallet for beginners. In this post I’ll review the different wallet features and why I think it’s one of the best wallets around.

Investors looking to select from a large menu of digital assets will likely find the one they are looking for on the Exodus platform. While Exodus does not provide two-factor authentication (2FA), users do have the ability to interact with a Trezor hardware wallet.

Users will maintain complete control over their assets, as Exodus is completely non-custodial.

Exodus supports more than 150 currencies, across seven separate blockchains. Users can buy and sell, as well as swap currencies on Exodus’ internal exchange. Additionally, Exodus’ partnership with FTX allows users to access the exchange directly from the Exodus app, facilitating the transfer of assets between the two.

Huobi Wallet / iToken

iToken Wallet is a professional multi-currency web3 wallet. It guarantees the asset security of global digital currency users from multiple dimensions and provides simple, convenient, safe, and reliable digital assets. Management services.

iToken Wallet Main Features

- Users have full control over their assets since they manage their own private keys.

- Support multiple patents for data security, such as security isolation and data encryption.

- Support multi-signature, multiple people jointly manage digital assets.

- Just takes one click to add and manage digital assets.

- Easy to manage multiple group addresses.

- One-click exchange is simple and easy to use.

Argent

Argent is a web3 wallet that is used to store cryptocurrencies and offers some lucrative benefits for prospective users of the platform. Argent is only available on the Ethereum blockchain and it was launched in 2020. The non-custodial web3 wallet allows the users of its platform to store all the cryptocurrencies based on the ERC-20, ERC-721, ERC-1155 tokens of the Ethereum blockchain. Argent wallet has been able to make a name for itself due to a host of reasons.

Other than being “up to 100X cheaper fees than Ethereum thanks to zkSync’s Layer 2 network”, with near-instant speed. A plus side of the web3 wallet is its easy user interface. Argent appeals to a large audience that wishes for a simple and secure wallet, even if it is not compatible with other blockchains. A variety of advanced features has also made this wallet stand out for experienced individuals who are much more familiar with DeFi and can make money on their crypto assets with the help of the Argent wallet.

Rabby

Rabby is an open source web3 wallet in your browser for Ethereum. 1. Designed for DeFi users with a smooth multi-chain experience. 2. Protect your assets with pre-transaction potential risk scanning. 3. Show you the upcoming balance change before you sign a transaction.

It supports up to 32 chains and enables multiple ways for signing transactions, from hardware wallets, to institutional wallets such as Fireblocks, and finally from mobile wallets like Metamask. Maintaining high security standards it enables users to seamlessly interact with DApps benefiting from a variety of DeFi services.

1inch

1Inch Wallet is a mobile wallet developed by Anton Bukov and his team of blockchain devs, creators behind the decentralized exchange (DEX) of the same name. The wallet is designed to provide investors with effortless access to the enormous DeFi market, and it does so by packaging a fast and secure web3 wallet with token swapping functionality provided by the 1Inch DEX aggregator into a light and portable mobile application.

It was a big selection of features: swap, play, NFTs, buy, send, store, browse.

Torus

Torus can be considered as a bridge between web 2.0 and web 3.0. Torus wallet offers a platform that helps connect with billions of web 2.0 users accustomed to mainstream OAuth logins. It acts as a gateway for easier decentralized ecosystems, blurring the line between web2.0 and web3.0. It is an everyday portal for Blockchain technology.Once onboard, Torus wallet users can access Ethereum, Polygon, BSC, and other Blockchain networks, providing access to information and cryptocurrency coin purchase options.

Token Pocket

Headquartered in Singapore, TokenPocket is a multi-chain wallet that supports multi coins. You can store, send and receive your Bitcoin (BTC), Ethereum (ETH), EOS, TRON (TRX), IOST, Cosmos and Binance (BNB). With its Web3 browser, you can interact with Decentralized Applications (DApp) and trade your ERC20 tokens, BTC and EOS in decentralized exchanges (DEX), play blockchain games directly inside the wallet. You can also get free airdrop, get your staking reward through some (PoS) mining pools and join the Decentralized Finance (DEFI) like MakerDAO.

TokenPocket supports the leading chains/cryptocurrencies such as Bitcoin, Ethereum, EOS, Polkadot, TRON, BSC, HECO, IOST, Cosmos, Binance, BOS, MOAC and Jingtum.

Phantom

Phantom wallet is a popular web3 wallet designed for users to interact with the world of DeFi and Web3. It allows users to securely store, send, receive and trade tokens and NFTs (non-fungible tokens) across multiple blockchains including Solana, Ethereum and Polygon. Users can leverage Phantom to access various decentralized applications (dApps) and DeFi (decentralized finance) tools directly within the wallet. The recently updated Android app boasts features like secure biometric authentication, built-in swapping for easy token exchange, and the ability to stake Solana (SOL) tokens for earning rewards. Phantom wallet currently has 2.54M downloads on online stores.

SafePal

SafePal offers a two-pronged approach to cryptocurrency management: a mobile software wallet and its signature S1 hardware wallet. The app, available for iOS, Android, and major browsers, allows users to store, send, and trade various cryptocurrencies and NFTs. Unlike many hardware wallets, SafePal’s S1 doesn’t directly connect to a computer or phone. Instead, it utilizes QR code technology for a secure air-gapped transaction confirmation process, adding an extra layer of security. The S1 boasts a high-resolution display for easy navigation and works seamlessly with the SafePal app for a comprehensive crypto management experience.

Summary

Covering all wallet services would require huge amounts of resources as the DeFi space remains on growing exponentially. Everyone is fighting to get a share of the pie when it comes to servicing Web 3 users. We saw some projects concentrate on the lower end of the spectrum by catering their products to retail and private individuals, while others develop products specifically based on financial institutions’ needs as they target bigger volume investors.

Web3 companies are only starting and we’re already seeing significant traction picking up in this ecosystem as it bootstraps to take over the future of the internet. Wallets are the gateway to Web3, meaning ensuring its safe and secure development and providing a variety of services will be detrimental to decide the fate of that future.